.webp)

Invoice payment terms explained: How to get paid faster and avoid delays

Did you know that nearly 44% of invoices in the UK are paid late, with small businesses owed more than £112 billion in overdue payments? If you run a business, that statistic may not surprise you. Late payments affect cash flow, create stress and take valuable time away from running your company. This is why clear invoice payment terms are so important. They make your expectations straightforward, reduce misunderstandings and help you avoid the long, tiring process of chasing overdue invoices or turning to debt collection.

This article from My Credit Controllers explains how payment terms work, how to choose the right ones and how they help you get paid on time without awkward conversations or long back-and-forth emails.

Key takeaways on payment terms

Clear invoice payment terms help you set expectations with your customers from the start. When customers understand when to pay, how to pay and what happens if they fall behind, the whole process becomes simpler. These terms also help you protect your cash flow and can reduce the chances of needing outsourced credit control or moving towards debt collection.

Here’s what this article covers

This article explains what invoice payment terms are, why they matter, the different types you can use, how to choose the right terms for your business and how to add them to your invoices. You will also find examples and answers to common questions at the end.

What are payment terms on an invoice?

Invoice payment terms are the conditions you give a customer to explain when and how they must pay you. They act like a short agreement that sits on each invoice. These terms normally include the due date, accepted payment methods, what to do if the customer wants to query the invoice and whether any discounts or extra fees apply.

Good payment terms set the tone for a smooth transaction. They help avoid confusion, remove guesswork and reduce the risk of unpaid invoices slipping into debt collection. When written clearly, they support both you and your customer, as everyone understands what is expected from the start.

Companies offer credit to customers for a number of reasons, allowing customers to place orders without immediate payment when they purchase goods or services. This helps customers buy what they need without having to pay the full amount upfront. Most often, credit is offered only to customers with a reasonable financial position. There are many forms of trade credit and businesses use a range of abbreviated codes on their invoices to show the terms agreed. One side effect of offering credit is that you sometimes have to remind customers when they fall behind. This is where having a strong credit control function becomes important.

Why your business needs the right invoice payment terms

The right invoice payment terms give you more control over your cash flow. When customers know exactly how long they have to pay, you can plan your spending with confidence. This matters whether you are a sole trader or a larger company.

Clear payment terms help prevent late payments and arguments. They also support the relationship you have with your customers by reducing the chances of misunderstanding. If your terms are predictable and written in simple language, customers are more likely to pay promptly. This reduces the amount of time you spend on follow-ups and lowers the chance that you will need outsourced credit control or more formal debt collection steps.

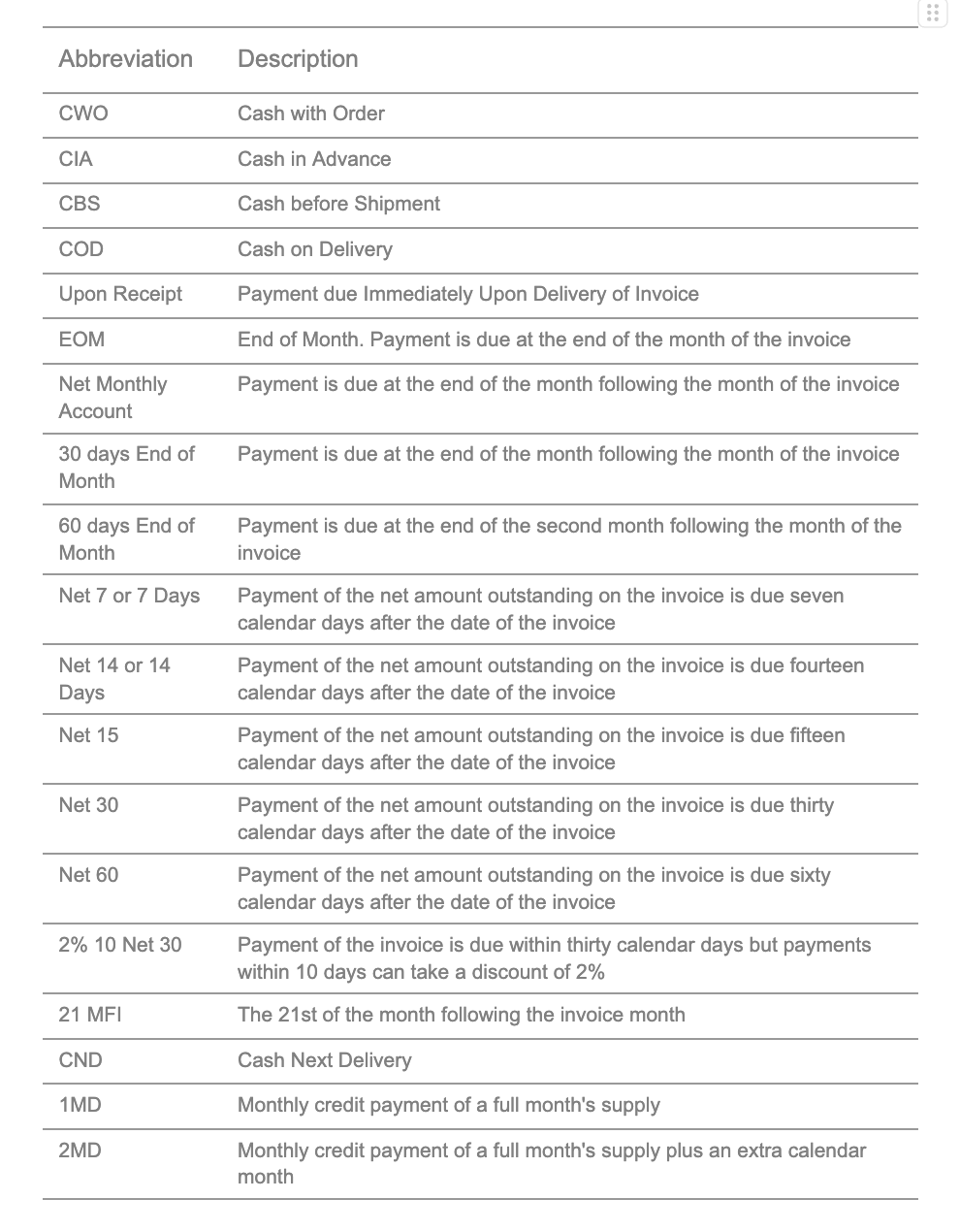

23 types of invoice payment terms every business should know

Understanding different payment terms helps you choose the right option for each customer. Below are some of the most widely used terms.

1. Cash In Advance (CIA)

Payment is required before work begins.

2. Cash Before Shipment (CBS)

Goods are shipped only after payment is received.

3. Cash On Delivery (COD)

Payment is collected at the point of delivery.

4. Cash With Order (CWO)

The full payment accompanies the order.

5. End Of Month (EOM)

Payment is due at the end of the month the invoice is issued.

6. Payment In Advance (PIA)

Payment must be made before any work is carried out.

7. Prompt Payment Discount (PPD)

A small discount is offered if the customer pays early.

8. Cash Against Documents (CAD)

Documents are handed over once payment is made.

9. Month Following Invoice (MFI)

Payment is due the month after the invoice date.

10. Net 7, Net 10, Net 30, Net 60 or Net 90

Payment must be made within the stated number of days.

11. 1% 10 Net 30

A 1 per cent discount applies if the invoice is settled within 10 days.

12. Interest invoice

Interest is added where payment is late.

13. Early payment

A general term for any arrangement rewarding quicker payment.

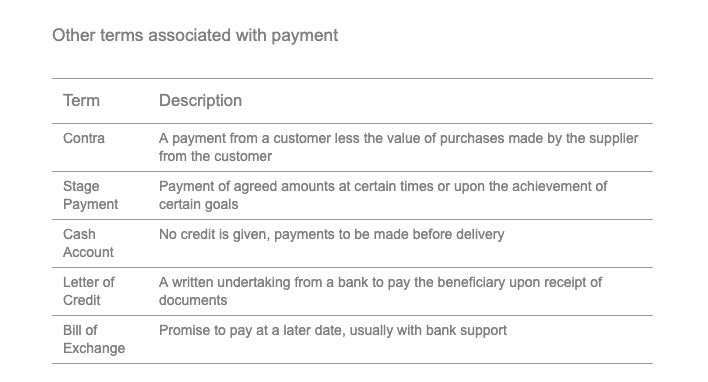

14. Contra payment

Amounts owed between two businesses are offset.

15. Terms of sale

The full conditions that apply to a transaction.

16. Payment plan details

Payments are spread across a number of agreed dates.

17. Payment method

The specific payment types you accept.

18. Shortened payment period

A shorter period is used to protect cash flow.

19. Upfront payment

A deposit is taken before work starts.

20. Overdue fees

Extra charges that apply once an invoice becomes overdue.

21. Net monthly account

Invoices are settled monthly rather than individually.

22. Letter of credit

A bank guarantees payment on behalf of the customer.

23. Bill of exchange

A written promise to pay on a certain date.

When to create or update invoice payment terms

You should revisit your invoice payment terms whenever your business circumstances change. If you are experiencing regular delays, it may be time to shorten terms or request deposits. If you begin working with a new type of customer or change your pricing structure, updating your terms can help shape clearer expectations. A review can also be helpful when you introduce new payment methods or begin using outsourced credit control to improve your cash flow process.

Cash flow forecast template

If you do not already use one, consider creating a cash flow forecast. This helps you see when money is due in and out and makes it easier to decide which payment terms suit your business best. A forecast can also highlight seasonal patterns or quieter months when quicker payments become more important.

How to choose the best invoice payment terms and conditions

Choosing the best invoice payment terms begins with understanding the financial rhythm of your business. If your outgoing costs fall shortly after you complete work, shorter payment terms might suit you better. It also helps to consider what is common in your industry. Some sectors use Net 30 as a standard, while others rely on deposits or staged payments.

Customer history plays an important part. Customers who have a strong record of paying on time may be given more flexibility, while those with poor records may be asked to pay upfront. Clear late payment fees can encourage prompt payment and protect your business when invoices slip behind. Invoice size also matters. Larger projects often require deposits or staged billing to reduce your risk.

How to write payment terms on an invoice

Good payment terms are written in clear, simple sentences. Avoid jargon and explain the steps plainly. Tell the customer when payment is expected, how they can pay, whether they qualify for any discounts and any fees that apply if they pay after the due date. It is helpful to give the name or email address of someone they can contact with questions. Clear wording reduces confusion and prevents disputes that may otherwise move closer to debt collection.

Example of payment terms on an invoice

Payment Terms: Payment is due within 14 days of the invoice date. A 2 per cent discount applies if payment is made within 7 days. Late payments may incur a 25 pound fee plus interest. Accepted payment methods are bank transfer or card payment.

You can adjust this example to suit your own business needs.

Common challenges with invoice payment terms

Many businesses experience delays because customers misunderstand the terms. Sometimes the terms are written in complex language, or they appear in small text where they are easily missed. Other challenges arise when the same terms are used for every customer, even when the level of risk varies. Without a consistent follow-up process, overdue invoices often remain unpaid for longer than necessary. At this point, companies sometimes need outsourced credit control or even formal debt collection.

10 best practices for handling your invoice payment terms

Begin by understanding the customer’s usual payment habits. Offer a couple of payment options so that customers can choose what suits them. Small rewards for early payment can motivate quicker settlement. Adding late fees helps customers understand that paying late has consequences. Shorter terms may work better when your cash flow has tight timings.

Polite language creates a better atmosphere during follow-up conversations. Sending invoices as soon as work is complete increases the chance of prompt payment. Tracking invoices closely allows you to follow up before delays grow into larger problems. Present your terms in a clear, simple layout so they are easy to understand. Finally, remain flexible when necessary. Some situations benefit from a temporary payment plan rather than pushing the customer towards debt collection.

Manage your invoice payment terms with automated accounting software

Automated systems allow you to send invoices immediately, keep track of unpaid invoices and send reminders at helpful intervals. This reduces the amount of manual work involved and helps you spot overdue payments early. Many businesses find that automation lowers stress levels and reduces the amount of time they spend chasing customers. It can also work alongside outsourced credit control to maintain a steady cash flow.

Why Clear Invoice Payment Terms Help You Get Paid Faster

In conclusion, clear invoice payment terms protect your business, support healthy cash flow and help customers understand their responsibilities from the start. When written in simple language and used consistently, they reduce arguments, lower the chances of late payment and limit the need for further steps such as debt collection. Choosing the right terms for each situation gives your business more stability, and following up in a structured way helps keep payments on track.

If you would like expert help improving your credit control process or reducing late payments, contact My Credit Controllers today.

.webp)

.webp)